Building Finance: Adaptive Building

Summary

In this long-awaited building finance article, I finally leave the building industry fallacy conversations and move into the forces of change. We will first cover how the finance world interacts with the rest of the world, explaining its relevancy along the way. We will then transition into the different facets of sustainable investing, positive and negative, and how one of them is particularly inclined to nudge the building industry into an ‘above and beyond minimum standards’ state with theoretical examples to drive the thought processes of Adaptive Building: site assessment and integrative design.

I will then continue to draw connections between the building industry and business decision making. What would happen to a CEO if they pretended like climate change doesn’t affect them and eventually does? Lastly, I would like to disclaim that when I speak of risk of a conventional building vs. an adaptive building I am not implying that conventional buildings carry an extraordinary amount of risk. I mean that an adaptive building is relatively less risky than a conventional build.

Building Finance

Ever since the dawn of capitalism, civilization has operated in a forward-thinking attitude. This attitude shows itself in the way we finance the construction of our modern world. To bring a product to market, companies and external raters speculate the profit potential of their new product or service (a valuation), and they source the necessary money by going into debt based on that expected future income. One must be able to predict and mitigate any future hiccups or crippling risks to the new product or service, or you risk losing the bank’s money, aka, you are unable to pay it back.

Despite financing being a common and practically universal strategy, the building industry has never walked in the shoes of the future, choosing to remain in the idea that cost effective and quick building is considered valuable. The world is changing, and the building industry will not be able to keep up with volatile weather unless it changes as well. We, as a society, are losing our ability to predict all of the physical risks to our built environment due to the changes in regional climate, as laid out in the State of Building Code article. The same kind of risk financers would like to understand.

Every year we experience ‘once in a lifetime events,’ whether it is a destructive wildfire, hurricane, drought or heatwave. I begin to wonder when we will start experiencing ‘once in a millennium event?’ The answer is, sadly, we already are, specifically some of the Pacific Northwest heatwaves. So, if the question of when has already been answered, we must ask ourselves what we are going to do about it?

While I would love to simply say “green building, green building, and some more green building,” I recognize that green building goes above and beyond in considering a ‘healthy space,’ and if we hope to drive the adoption of green building we need to think beyond Chicken Little screaming the sky is falling. The building industry will start to see more adaptive buildings spurred by financers’ risk assessments, as a compromise between cost effective building and the various foci of green building, many of which do not impact structural integrity. There are many routes the industry can take to arrive at the adaptation destination, but I believe “show me that this money I am giving you won’t be wasted on a rushed build” will be the most powerful and inversely simple route.

Positive vs. Negative

To understand why I expect this to happen, we must first understand how financers operate, specifically, how they protect their own assets/money. To protect themselves, financers have an incredible ability to rate risk, and the notion of sustainable investing grew around some of the exceptionally low risk opportunities they uncovered. Sustainable low risk opportunities do not follow the conventional wisdom of high-risk, high reward. When it comes to physical items that can only degrade in quality over time, lowest risk can mean the highest reward, i.e., minimal degradation.

There are two categories of sustainable financing: positive and negative. At the moment, negative financing is the most popular type where the goal of financers is to avoid high risk situations, such as investing in fossil fuels, as compared to positive where financers judge potential growth/upside (otherwise known as impact investing). While this association is by no means 100% accurate, positive vs negative financing can be understood as venture investing vs institutional investing respectively. Understanding that negative financing is the most popular, and objectively, the easiest type of sustainable financing is imperative for this analysis. Unless a new build is piloting a new ‘wonder material,’ then venture investors will likely remain unassociated with the average players within the building industry. This means that the average business interaction a building industry stakeholder will have will be with a minimal risk seeking finance firm/person.

Adaptive building adoption will be driven by negative sustainable financing because financers hold most of the leverage, and decisions do not need to rely on confidential information. Negative financing allows objective third party data to enter decision making. A financer can tell a developer that they want the new build to be stronger/less risky or go kick rocks. Even if the developer has only done quick conventional builds, they can go outside of their organization to find the best practices/procedures to accommodate that financier’s checklist. Which means, no one needs to be an entrepreneur in these situations.

Building stronger buildings and wasting less time, money, and resources repairing weak ones is not waiting for some unrealized technological innovation; it is just waiting for the threat of kicking rocks. Knowing change is that “simple” is important because you get the sense that the building industry believes green building adoption will come from positive financing when looking at the various data points of the Dodge Data and Analytics World Green Building Trends 2018 report 3. You can consider it the limitations of the report, but a large majority of questions revolve around mitigation strategies and positive financing. Examples are reducing energy and water consumption by making the building more efficient with new technology. These actions reduce a building’s negative impact on the environment (mitigation) and are often sold/marketed by their upside of saving money due to consuming less resources (positive financing).

However, new technologies making a home more efficient does not influence total building procedure. More specifically, their inclusion in a build does not influence the structural integrity. They are merely solving a segment of a building’s impact, while we still neglect the impact of construction’s “quick and cost effective” intrusion on the environment and consumption of resources (in the frame of choosing to not build beyond minimum standards, yet still calling it a 70–100-year building).

Preservation of Capital

Negative sustainable financing will be the force to reckon with because financial institutions hold the leverage and stand to benefit from facilitating adaptive buildings. Firstly, they have an extraordinary amount of freedom choosing which projects/builds they want to finance and which ones they want to turn away. While I recognize investing in adaptive properties isn’t a core function of many firms… yet; I also recognize that all it takes is a few players to find success in funding adaptive building projects to form a new industry standard. These first few revolutionizing players will likely cite minimizing risk within their portfolios as a major contributing factor to their actions, which means, being more sustainable is not the primary driver for them.

The biggest risk to an investor/loan provider is the risk of default. There can be many reasons why a person or company may default on their loan, but in the world of extreme financial planning such reasons are, by in large, random and unnatural. Imagine situations similar to last December’s series of tornados wreaking havoc in the relatively tranquil areas of Tennessee, Arkansas, and Kentucky. The people who did not have the proper or full coverage insurance for the event now have to repair their homes out of pocket which likely affects their ability to pay their mortgage.

Even extreme weather prone areas, where the building code would have to and “does” accommodate stronger storms, historically experience an increase in mortgage defaults from extreme weather. CoreLogic’s 2021 Hurricane Report found a 4.7% and a 7.3% increase in mortgage delinquencies in Houston, TX and Panama City, FL after hurricanes Harvey and Michael respectively 4.

How can financers get around this risk?

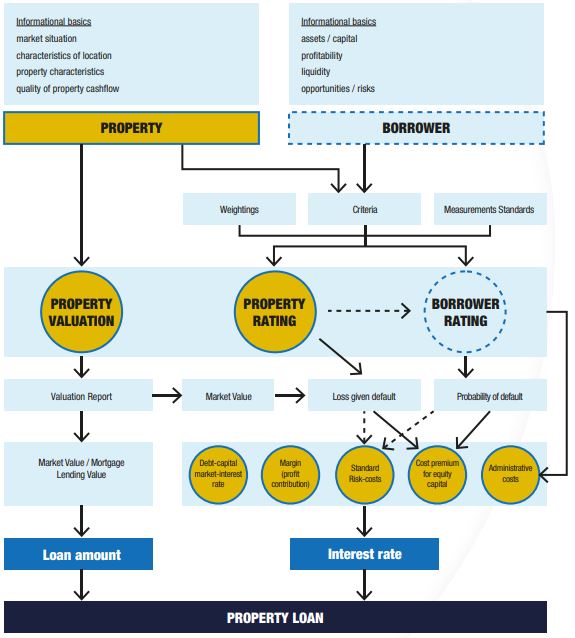

Financers can provide better loan rates [and insurers for their respective rates] for adaptive buildings knowing that decreases the risk of default. Obviously, the correlation of adaptive buildings equaling a lower risk of default must be verified first. Nonetheless, looking at the diagram from UNEP’s (2014) report below, you can see two opportunities where adaptation can impact the risk of default 5. First, with the property rating where the increased time/effort required, and benefit provided from adaptive buildings can score high as a high-quality build. Second, with the borrower rating where builders who have a plethora of high-quality buildings proven to stand the test of reality can achieve financial benefits for their expertise and holistic thinking.

Lützkendorf (2014, May)

Lützkendorf (2014, May)

Both of these two ratings impact two quantitative risk metrics that directly impact the interest rate: “loss given default” and “probability of default.” This can be a very impactful adoption method as the world moves into a high interest rate environment. As the cost of capital goes up, banks will likely move to support less risky projects.

“If climate-related risks like extreme weather events become high, the public sector and the insured may need to take more risk. This could be in the form of investment in higher protection standards such as flood defenses or higher risk retentions. The warmer it gets, the more likely challenges for insurability arise.” ~ Allianz Sustainability Report 2021

A portfolio of adaptive buildings is not required, as long as you can accurately track building risks and the measures taken to avoid them, but we all understand the benefits of having hard and relevant reviews when shopping. Additionally, Dodge Data & Analytics World Green Building Trends 2018 points out that builders doing the majority of green builds (regardless of certifying) are relying on the certification process less and less across many projects 3. This is an evident factor of expertise and efficiency, and where the builders who first move into this adaptive space can really excel.

In turn, contractors with an attractive borrower rating will have proven themselves to the standards of the finance firm. And because their work has been proven effective to the institution, the building should receive a low probability of default and a potentially non-existent ‘loss given default’ because no matter what the building is used for, it is safe and strong, it will be inhabited, and it will make money.

Furthermore, the principles of adaptive building: a site assessment paired with integrative design, can serve to inflate any project’s property value. Not only would these principles provide an in-depth assessment and plan that can contribute to the value report, but this is also where higher risk builds/hazardous zone development can show the thoughtfulness of adaptive building. Keep in mind that this is extremely theoretical. A financer must be able to see the value of say: one project with an 8.3% premium over another comparable project because it accurately describes the site’s risks and how the premium is spent to implement above and beyond safety measures.

In the end, the adaptive building will simply receive better interest rates due to its ability to minimize risk for the lenders. Considering the meteoric rise of BlackRock’s involvement in sustainability and mobilization of the financial industry to solve the climate crisis within the last few years, this is only a matter of time.

A Precursor: Climate Risk Reporting

Climate change is here to stay. Due to this fact, and the future orientation of the finance industry, many enterprises are starting to report how the risks propagated by climate change could affect their company’s profitability. This move is not directly related to the world’s ‘sustainability awakening;’ it is a simple measure of protecting the credibility and integrity of the financial industry’s firms and credit evaluations. The stock market is based in speculation for future growth, much like how business loans are granted based on the potential for future profit. Companies could face serious misinformation lawsuits, or stock devaluations if they exclude climate risk and those risks come to fruition.

In a similar fashion, I not only expect climate risk reporting to find its way into the building industry, but that it is also THE thought procedure builders consider as they survey their construction site during the site assessment and integrative design processes. How do we expect these conditions to change in the future? What are we going to do about it?

For example, a builder states, “this building site is not in a special wind zone or located in an area with the potential for high wind speeds, but since the site sits at a higher elevation relative to most of the town, and it is the most vulnerable building to any increase in the region’s wind strength, we will make the building more resistant to wind than expected.” Or “the site maintains a relatively low rate of rainwater diffusion that accommodates the current natural rainfall patterns, but since the site is located in a humid area, which we expect to have increased downpours due to the warming of the climate, we will construct a dry pond on the property.” Now financers know that someone still paying their mortgage is less likely to default due to having to pay for potential flood damage. Both of these scenarios recognize that our buildings will live longer than current weather patterns, and both of these scenario’s actions would be absurdly expensive if done post construction relative to during construction.

“market pricing will also reflect perceived future risk to the property, surrounding infrastructure, residential properties and the increasing costs associated with insurance.” ~ Nuveen 2021 ESG Report

We will never know how the changes in regional climate will change future weather patterns with complete certainty. However, we are able to understand what each building site is vulnerable to so that we may proactively adapt to any potential future where that weakness is hit from the start.

Relevant Changes to the Finance Industry

The SEC released a proposal to standardize and mandate climate risk reporting for investors on March 21st, 2022. In the time of writing this, the proposal is in its “open for discussion” period, so it isn’t fully ratified. However, beyond the political opinions involved in the discussions, opinions from investors have been overwhelmingly positive. In the words of Dr. Karthik Balakrishnan, “this [mandate] highlights an important distinction between carbon accounting and transition planning 2.”

While this does not directly affect the private building industry, it is entirely likely this will still be influential to the flow of information surrounding our physical and financial environments. Specifically, I would like to simplify “carbon accounting” and “transition planning” into ‘how many’ and ‘what and why’ questions respectively. Climate risk reporting, in a surface level generalization, has primarily been company’s declaring how their operations contribute to climate change providing, almost solely, quantitative data. Now the SEC is telling companies with climate pledges they should prepare to explain ‘what are you doing to hit your impact goals and why specifically that?’

Corporate leadership will face an inflection point for climate action much like how builders will for doing more to go above and beyond standardized building code. With the potential SEC mandate, CEOs could play dumb and pretend to be ignorant to specific climate risks and continue to avoid making climate goals. However, as a leader to an entity many people throughout the public have money invested in, ignorance is strictly and only incompetence… it’s a CEO’s job to know every future risk and plot a strategic course ahead.

There will be no greater way to ruin your brand’s reputation then to pretend we live in a different reality where the risks to our health and financials are 100% represented by the past. While individual scandals can have wider, but unlikely, implications to a brand; playing dumb with the climate crisis will put your brand on the wrong side of ‘Us and Them’ as the demand for action grows in correlation to the amount of people suffering climate crises.

On top of all of this, four days after the proposal release, Treasury Secretary Janet Yellen would speak on the negative economic impacts associated with the war in Ukraine’s effect on natural gas prices 7. While her comments are pro-renewable energy investment, they are strictly based in financial considerations. She essentially dismisses the villainization of ESG’s underlying presence in the Russian sanctions, specifically S&G (Social & Governance). Her argument is that the moralistic sanctions on Russia are not the cause of the gas prices hurting the average American’s wallet, but the fact that the United States did not invest in renewables “rapidly enough.” By remaining as a fossil fuel-based economy, the United States is at the whims of the global natural gas market when investments in local renewable energy would insulate the United States citizens from global price swings. The more you rely on a geo-political sensitive commodity, the more you put yourself at the mercy of other countries actions. In my opinion, Janet Yellen’s remarks can be broken down to the US playing dumb for too long, and if the US was a company, the CEO would have been ousted.

Zooming Out

I understand this has no direct implications on the building industry, but these developments give us a good sense of the attitudes and opinions of the individuals in the upper echelon of the United States’ finance industry.

These developments prove how long-term considerations of the environment and geo-politics are increasingly being tied to financial health and considering the building industry is 40% of the worlds carbon emissions and a fairly large consumer of natural resources, it won’t be left alone.

Sources Cited:

1 Allianz. (2021). Allianz Group Sustainability Report 2021. Allianz. Retrieved September 16, 2022, from https://www.allianz.com/content/dam/onemarketing/azcom/Allianz_com/sustainability/documents/Allianz_Group_Sustainability_Report_2021-web.pdf

2 Balakrishnan, K. (2022, March 31). The SEC’s Climate Disclosure Rules will require companies to plan, not just measure [web log]. Retrieved from https://www.actualhq.com/blog/the-secs-climate-disclosure-rules-will-require-companies-to-plan-not-just.

3 Jones, S. (2018). World Green Building Trends 2018. Dodge Data & Analytics.

4 Larsen, T., Jeffery, T., Turakhia, R., & Moore, D. (2021). 2021 Hurricane Report. CoreLogic.

5 Lützkendorf, T., & Lorenz, D. (2014, May). Sustainability Metrics. United Nations Environment Programme Finance Initiative.

6 nuveen. (2021). ESG report 2021-2022. nuveen. Retrieved September 15, 2022, from https://documents.nuveen.com/documents/global/default.aspx?uniqueid=28352048-a550-4ee2-88c5-fe55356287bd

7 Schoifet, M. (2013, August 19). Stilt houses in Greenwich, Conn., foreshadow impact of new flood maps. Insurance Journal. Retrieved September 19, 2022, from https://www.insurancejournal.com/news/east/2013/08/19/302115.htm

8 Sorkin, A. (2022, March 25). Treasury secretary Janet Yellen: ESG Movement is not creating our energy problems. CNBC. Retrieved September 15, 2022, from https://www.cnbc.com/video/2022/03/25/treasury-secretary-janet-yellen-esg-movement-is-not-creating-our-energy-problems.html

- Filed Under: Advocacy

- ( 3847 ) views

Clayton is a Bentley University Alumnus. He became increasingly involved in environmental impact work throughout his tenure at Bentley. Much of his professional experience is working in the home energy industry. He served as a marketing intern and technician for a local solar company, and worked for the Mass Save Program’s quality assurance company, Abode EM. Recently, Clayton was inducted into the Millennium Fellowship, became LEED Green Associate Certified and he will be working at Schneider Electric as a Sustainability Consultant come June 2022.

- ( 0 ) Ratings

- ( 0 ) Discussions

- ( 0 ) Group Posts

Reply/Leave a Comment (You must be logged in to leave a comment)

Connect with us!

Subscribe to our monthly newsletter:

Greenbuild Report Out, 2025 Nov 12, 2025

Greenbuild Report Out, 2025 Nov 12, 2025

Sponsored Listings

Related Posts

-

-

-

-

Making Green Sustainable... Again Apr 20, 2020

-

Are you a sustainability rockstar? Sep 09, 2018

Not a Member Yet? Register and Join the Community | Log in